Business and financing models

The transformation to electrified road logistics creates a need for and opportunities to change existing business models. New actors and roles will be introduced. Within REEL, the parties work together to explore these needs and opportunities, as well as the development of data and recommendations for competitive and socially beneficial solutions.

This is done by studying the demonstrations that are taking place and discussing with the participating parties in REEL. Other related projects in Sweden and internationally are also studied and we learn from how business and financing solutions are developed in other countries.

What issues are the basis of our work?

- What factors and barriers are dimensioning for business model approaches in relation to logistics application for the various subsystem actors?

- How can the business risk be distributed among the players in the value chain in order to be able to efficiently and profitably establish and operate electrified logistics flows and enable a significant proportion of Sweden's total logistics flows to be electrified?

- How can business economics models be designed to provide players in Sweden with simulation and knowledge support in the implementation?

- What new actors can be introduced to the system?

- What are the possible financing models for scaled-up regional electrified logistics systems and how are they designed?

Companies in REEL

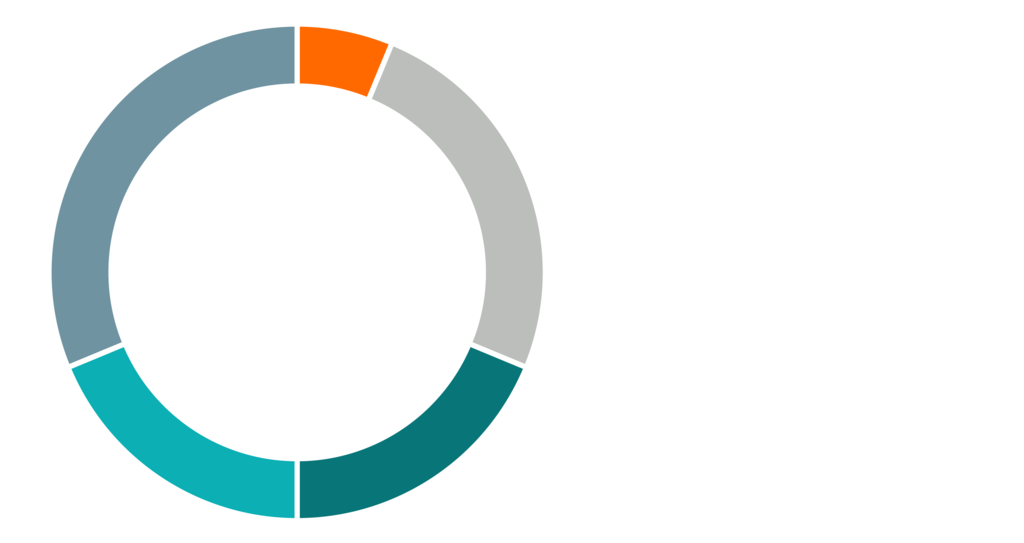

The turnover figures for the participating companies in REEL that have provided information to this report are presented below. As seen, there is a large spread when it comes to turnover. Some of the companies are traditional hauliers where transport accounts for the largest share of the turnover, while some are national distributors of e.g., food, and chemicals where transports only accounts for 10-15% of the total turnover.

Turnover in Sweden

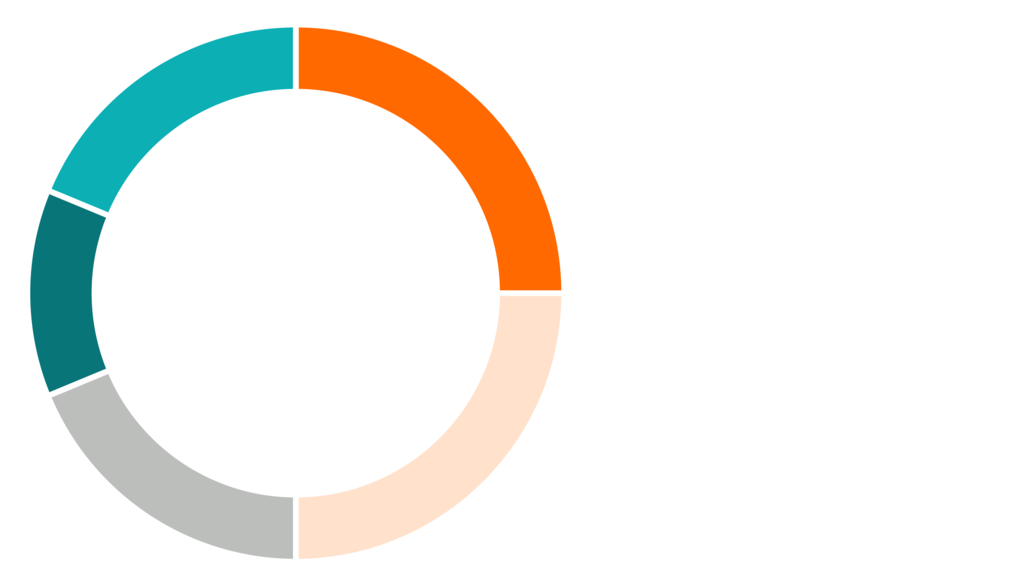

The total size of the own owned fleet of HDVs for the companies are presented below. Companies with large fleets and multiple logistic flows emphasize that it has been easy to find assignments where electric trucks are well suited. Smaller actors have been able to handle this as well although becoming more dependent on longer contracts with the customers in order to manage the uncertainties.

Number of HDVs in Sweden

How does the electrification of trucks affect the transport contracts?

The operation of the electric truck poses new ways of thinking in regard to the contracts between carriers and transport buyers. As utilization of the electric trucks is in its early days, there are some uncertainties. The residual value of the vehicles is hard to estimate as second-hand market doesn’t exist for the electric trucks at this stage. The degradation of the batteries, which is expected to be the most important factors for the residual value of the vehicles, is yet to be examined as the electric trucks have been put into operation quite recently.

In order to cope with these uncertainties, most of the participating transport companies in REEL see a need to increase the length of the transport contracts with their customers in order to ensure the utilization of their electric vehicles. At this early stage, implementation and operation of an electric truck often requires thorough preparations with the customer, and a customer willing to explore the new technology together with the transport company. If the transport contract is short, it might take time before the next assignment for the truck is found, resulting in the truck standing still and thus becoming a financial burden. Historically, the participating companies have applied contract lengths spanning mostly from 12 to 36 months for conventional transports (with some exceptions). Most companies see a need to increase the contract length to an interval between 36 to 60 months for electric transports. Such contract lengths have been applied for REEL transport flows. For some transport segments even longer contracts lengths are desired.

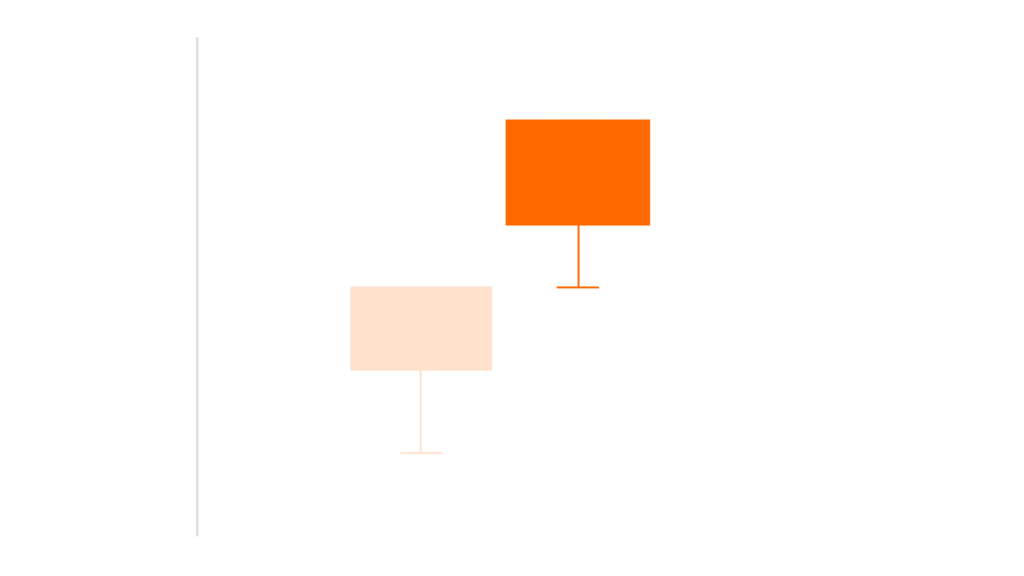

The participating companies' intention to change their transport contracts

Contract length applied historically for conventional transport solutions and intended length for electrified solutions [years]

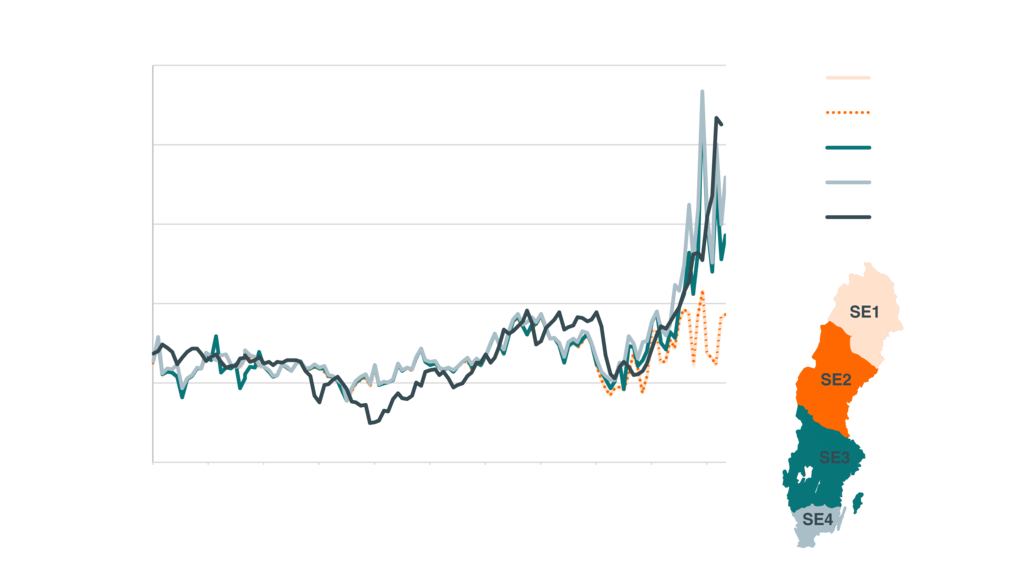

A common way to manage cost fluctuations with regards to driver’s wages, fuel price, maintenance and tires is to bind the transport contract to an index adapted for the specific transport assignment, e.g. DMT-T08. Currently, no index for electric energy prices to transport exists. Such an index is desired by a majority of the transport companies in order to reduce their risk as the energy prices are becoming increasingly volatile (see graph below). There are examples of models to handle this used by the actors, one is to separate the cost for the vehicle and the driver and pay for the charging separately.

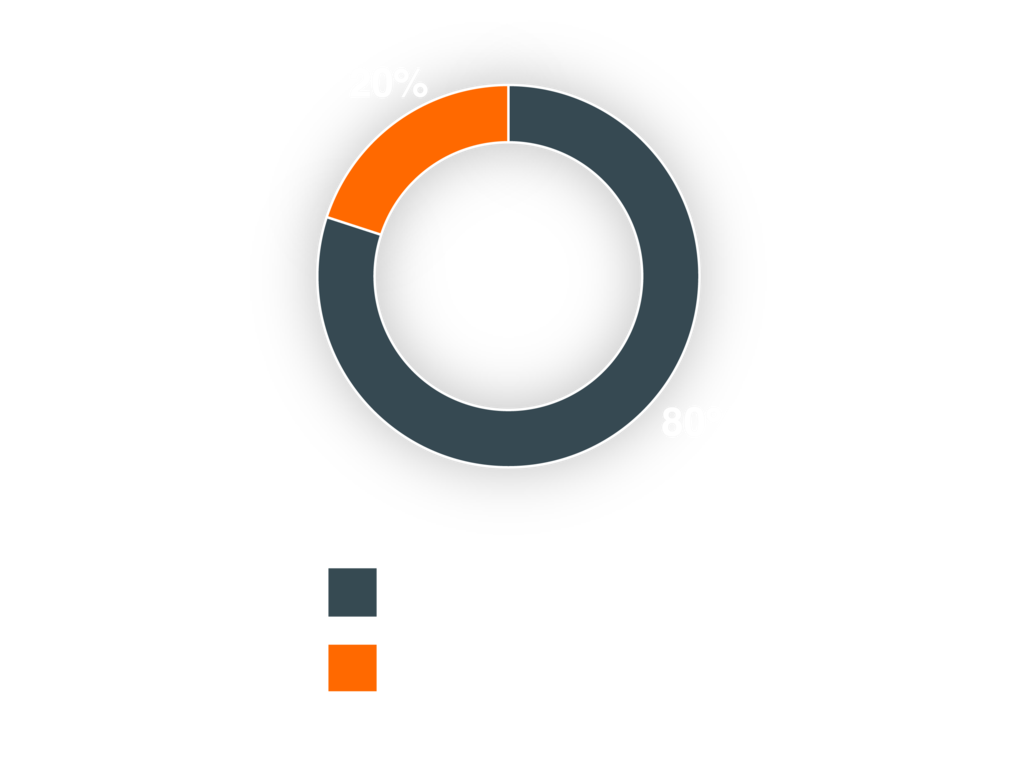

When asked, if the companies intend to change the price towards their customers, 44% of the companies state that they do intend to change it, 38% do not and 18% are unsure. A number of companies that have increased prices for the electrified cases have also mentioned following price increase intervals that they have applied: 5-10%, 15-20% and up to 50%. Some actors chose not to mention any intervals. When discussing potential price increment for the contracts in 5 years from now, the majority of actors expect the prices to be same as current prices for contracts performed with conventional vehicles, or lower. Companies that did expect higher prices in 5 years, stated intervals 5-10% and up to 20%. The argument for the higher contract prices were the higher investments and leasing fees for the electric trucks, uncertainty in price for charging at public locations and uncertainty regarding energy prices. Companies that do not believe that contract prices should and will be higher expect the price for the electric trucks to gradually decrease and also expect the price for fossil fuels to increase in the future, which will improve the total cost of ownership for electric fleets.

Price development for diesel and electricity in electricity price area SE 1 - 4

Charging infrastructure

In all cases, presented in this report, the investment in chargers and related infrastructure has been done by the participating companies i.e. no real-estate companies or CPOs have made the investments. The utilization rate of the installed chargers is 20-30% for high power chargers (>150 kW) and around 35-50% for low power chargers (<49 kW).

95% of the actors forecast that they will still own and operate their own infrastructure in 5-years from now, while 5% are investigating the possibility of transferring the ownership and operation to a third party and instead purchase charging as a service. All actors also state that they will be able to provide charging to other logistic actors that operate on their premisses. Notably, the haulier network organizations, freight forwarders, and food distributors consider charging as an important service for them to provide to their hauliers. Approximately 95% of all energy charged is assumed to be charged at either transport company’s own or at customers’ non-public chargers in the next five years. However, 4 out of 17 actors note that this is highly dependent on the development both with regards to maximum range of the vehicles and pricing for public charging. If electrified long-haul transports will be proven to be possible, the importance of public charging is expected to increase.

A majority of the actors believe that the local grid capabilities will be a limiting or a very limiting factor in the near future for many of their terminals and/or depots. It is regarded as one of the main risks for their strategies of replacing the fleets. In order to cope with this challenge, most actors are currently investigating solutions for local energy production and storage. Energy and power management are seen as key elements and will be new capabilities that the actors need to master.

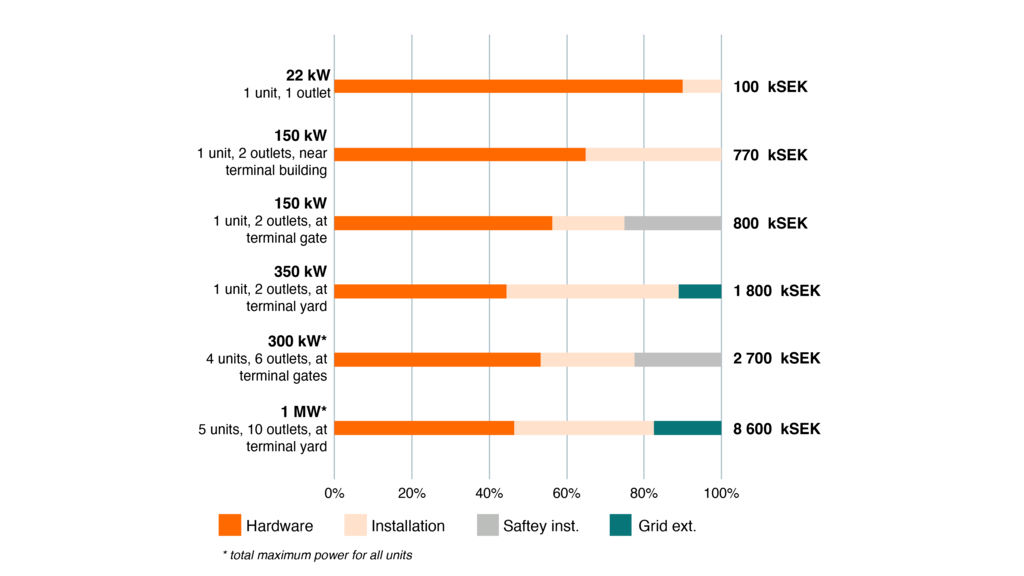

The cost for charging infrastructure solutions varies a lot with the local pre-conditions with regards to current grid connection and need for upgrade of electrical components in the facilities. Below, some of the cases and their costs split are presented:

What financing models are used and will be used for electric trucks?

A majority of the actors have chosen to use operational leasing as the financing model for their first battery electric trucks. Actors are unsure of the performance of the first generation trucks for example with regards to battery degradation. Actors also believe that specifications for these trucks will be outdated in a few years time due to the rapid development in the field. Thus, operational leasing is used to minimize risk of low residual value. The actors who forecast that they will continue to use operational leasing in five years from now, believe that these arguments apply will be prevailing at that point in time.

However, a shift from operational leasing to cash payment is noted in a five years’ time. Actors that prefer this model state that they benefit economically through either cash payment and/or financial leasing. They expect that the performance of vehicles will improve in the coming years and that battery electric trucks will have a longer lifecycle than conventional trucks. Therefore, actors would like to keep the vehicles as long as possible in their own operation, some state up to 12 years, succeeding by shifting routes and operation as the batteries degrade.

Multiple actors state that the financing of trucks will be a hurdle for small hauliers. A solution to this is that some of the larger actors and the haulier network organizations see is by them taking ownership of trucks and lease those to smaller hauliers.

Do you want to know more?

Magnus Karlström